>

>

Shariah Complaint Annuity Plan and the Issue of Hibah with Consideration

Generally, annuity is defined as a retirement scheme whereby the insurance company provides a series of payments at regular intervals from a fixed date until the death of the annuitants. In return for this benefit, the annuitants will have to pay a certain sum of money, known as the purchase price.

Despite various retirement products in the market offered by either conventional insurance or the government, there is no Shariah-compliant retirement annuity plan which satisfies the features of a defined benefit plan in which the participants will receive regular payouts starting from either retirement age or a deferred period (if applicable) until the participant’s death.

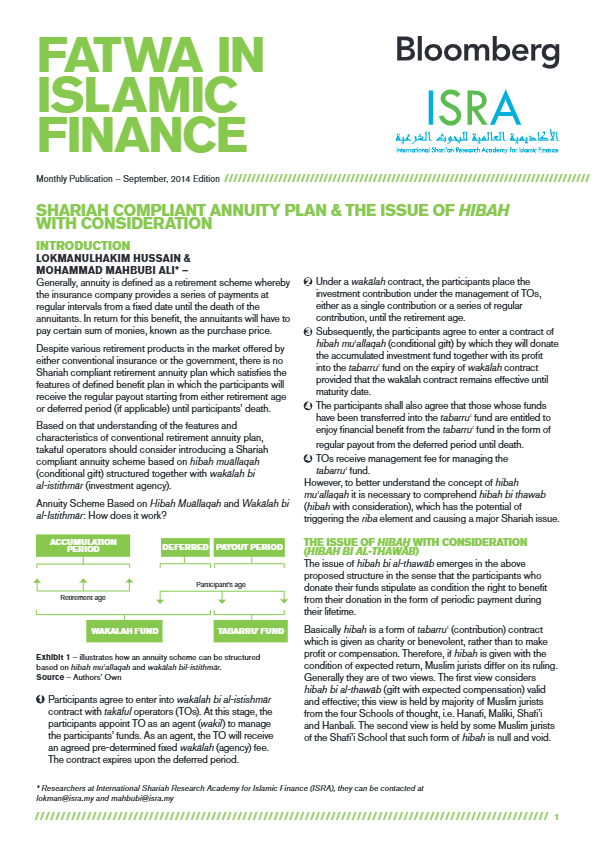

Based on that understanding of the features and characteristics of a conventional retirement annuity plan, takaful operators should consider introducing a Shariah-compliant annuity scheme based on hibah muʿallaqah (conditional gift) structured together with wakālah bi al-istithmār (investment agency).

Annuity Scheme Based on Hibah Muʿallaqah and Wakālah bi al-Istithmār: How does it work?