The past few issues of the bulletin have successfully published a series of articles introducing different structures of sukuk based on different underlying Shariah contracts, ranging from simple murabahah sukuk to istisna and ijarah sukuk. This issue will feature another sukuk structure based on the musharakah contract, which is one of the most commonly used structures in the Islamic market. This article, similar to the preceding writings on sukuk, primarily aims at providing an overview on musharakah sukuk and highlights some Shariah issues raised concerning this type of sukuk along with any resolution issued regarding it.

The history of musharakah sukuk globally began with the first issuance by Sarawak Shell Bhd in 1991 based on the concept of musharakah mutanaqisah (diminishing partnership). It was then followed by other issuances such as the one issued by The Islamic Religious Council of Singapore (Majlis Ugama Islam Singapura–MUIS) in 2001 and 2002. Since 2005, the sukuk market has been witnessing the spur of musharakah and other equity-based sukuk (EBS) namely mudarabah and wakalah, particularly in the Gulf Cooperation Council (GCC).

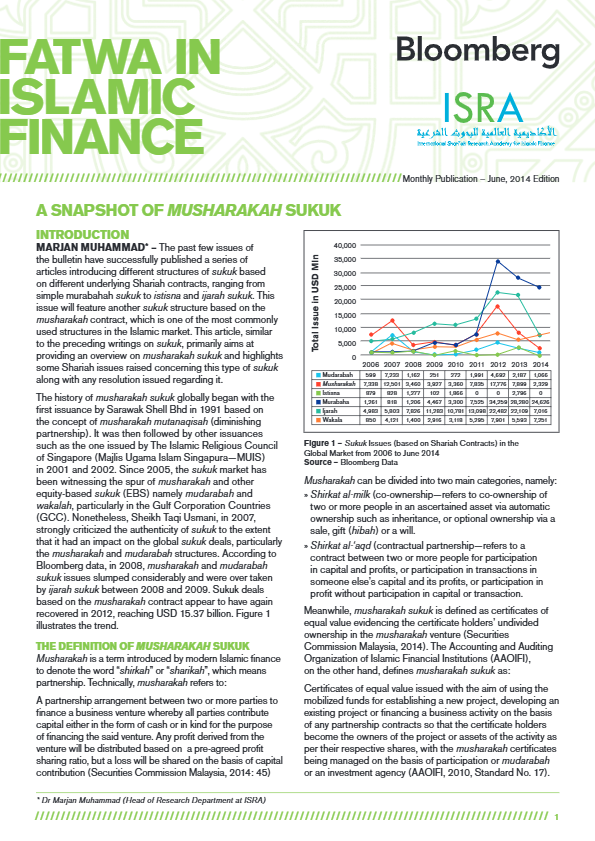

Nonetheless, Sheikh Taqi Usmani, in 2007, strongly criticized the authenticity of sukuk to the extent that it had an impact on the global sukuk deals, particularly the musharakah and mudarabah structures. According to Bloomberg data, in 2008, musharakah and mudarabah sukuk issues slumped considerably and were overtaken by ijarah sukuk between 2008 and 2009. Sukuk deals based on the musharakah contract appear to have again recovered in 2012, reaching USD 15.37 billion. Figure 1 illustrates the trend.