>

>

IRP 68 – An Empirical Study of the Effectiveness of the Shariah Governance Framework (SGF 2010)

Malaysia has placed great emphasis on strong structure and corporate governance values of Islamic financial institutions (IFIs) operating Islamic financial business in order to ensure conformity and adherence to Sharīʿah principles. Not only that, the legal structure of IFIs in Malaysia is significantly ahead of other countries, and the corporate and Sharīʿah governance framework is undoubtedly well in place, making Malaysia the role model for the world’s Islamic financial industry. The Sharīʿah governance aspect has always been part of the legal infrastructure starting from the initial establishment of Islamic banking and finance in Malaysia. This is evidenced by the incorporation of the requirement of Sharīʿah compliance vis-a-vis Sharīʿah governance provisions in the Islamic Banking Act 1983 requiring Islamic banks to include mention of the Sharīʿah compliance of their operations in their articles of association. At that stage the Sharīʿah compliance aspects of Islamic financial institutions were the prerogative of the Sharīʿah committees appointed by the respective IFIs. This was followed by the introduction of the Guidelines on the Governance of Sharīʿah Committee for Islamic Financial Institutions, known as Garis Panduan Syariah (GPS1), in 2004. The Guidelines issued by the Central Bank of Malaysia (Bank Negara Malaysia/”BNM”) set out the rules, regulations and procedures for the establishment of a Sharīʿah committee; defined the role, scope of duties and responsibilities of a Sharīʿah committee; and provided guidance to IFIs on the relationship and working arrangement between a Sharīʿah committee and the SAC of Bank Negara Malaysia.

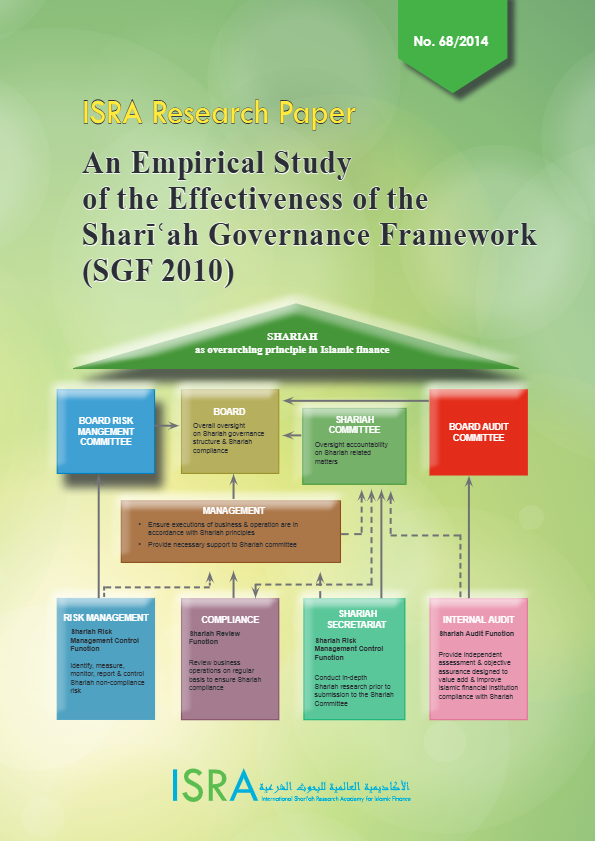

The commitment of BNM to continuously enhance the Islamic finance industry was further evidenced by the introduction of the Shariah Governance Framework for Islamic Financial Institutions (SGF) which was introduced in late 2010. The framework took effect on January 2011. These new guidelines enhance the functions of the Sharīʿah committee and emphasise the responsibility of all stakeholders in ensuring that the operations of the institutions are conducted in a Sharīʿah-compliant manner. The significant aspect of the new guidelines is that the stakeholders of Sharīʿah compliance have been widened to include the board of directors and management of the IFIs in addition to the Sharīʿah committee. This framework also sets out the requirements on the proper Sharīʿah governance structures, processes and arrangements to ensure that Sharīʿah compliance is being dutifully observed by the IFIs. As such, the guidelines put a strong emphasis on the functions of Sharīʿah review, Sharīʿah audit, Sharīʿah risk management and Sharīʿah research.

This study was conducted almost two years from the date when the SGF 2010 was effectively enforced. It seems that this is the right time for a study to be conducted to analyse the effectiveness of its implementation, which is imperative for sustainable development of Islamic financial institutions in Malaysia. The expected outcome of this study is that it will shed light on the practical problems involved in implementation of the new framework, provide insight on how to curb problems, and contribute towards development of Islamic financial institutions in Malaysia.

This study was conducted in order to identify the level of readiness among IFIs to adopt the SGF 2010, to identify the IFIs’ efficiency of resources and infrastructure for adoption, and also to identify the IFI’s general expectation on significant effects of the implementation. The study utilises a survey method through face-to-face interviews using a set of questionnaires to collect data. The interviews were conducted from 9th July to 15th September, 2012. The sample respondents are persons with Sharīʿah-related functions in IFIs from among the Sharīʿah committees, the management and the Sharīʿah officers. The data are evaluated based on the Likert scale to measure the level of readiness of the IFIs, their resource effectiveness and manpower efficiency, and also the IFIs’ perceptions of SGF 2010’s significant effects on their respective institutions. The respondents’ responses were analysed based on their awareness of the Sharīʿah governance framework; their effective utilisation of resources and efficient manpower; and their perception on advantages of SGF 2010 and the constraints that they face in adopting the SGF requirements.

The overall findings of the research are that IFIs have gotten ready for the SGF 2010 by effectively gearing up their infrastructure and resources for full implementation of the SGF requirements. Despite some minor challenges, the IFIs have shown positive commitment to full compliance with the Sharīʿah governance framework. These encouraging phenomena will boost the integrity of Malaysian IFIs, enhance stakeholders’ confidence, reduce Sharīʿah non-compliance risk, and thus contribute towards maintaining financial stability of the Malaysian Islamic financial industry.

Keywords: Sharīʿah Governance Framework, Malaysia, Islamic finance industry, implementation